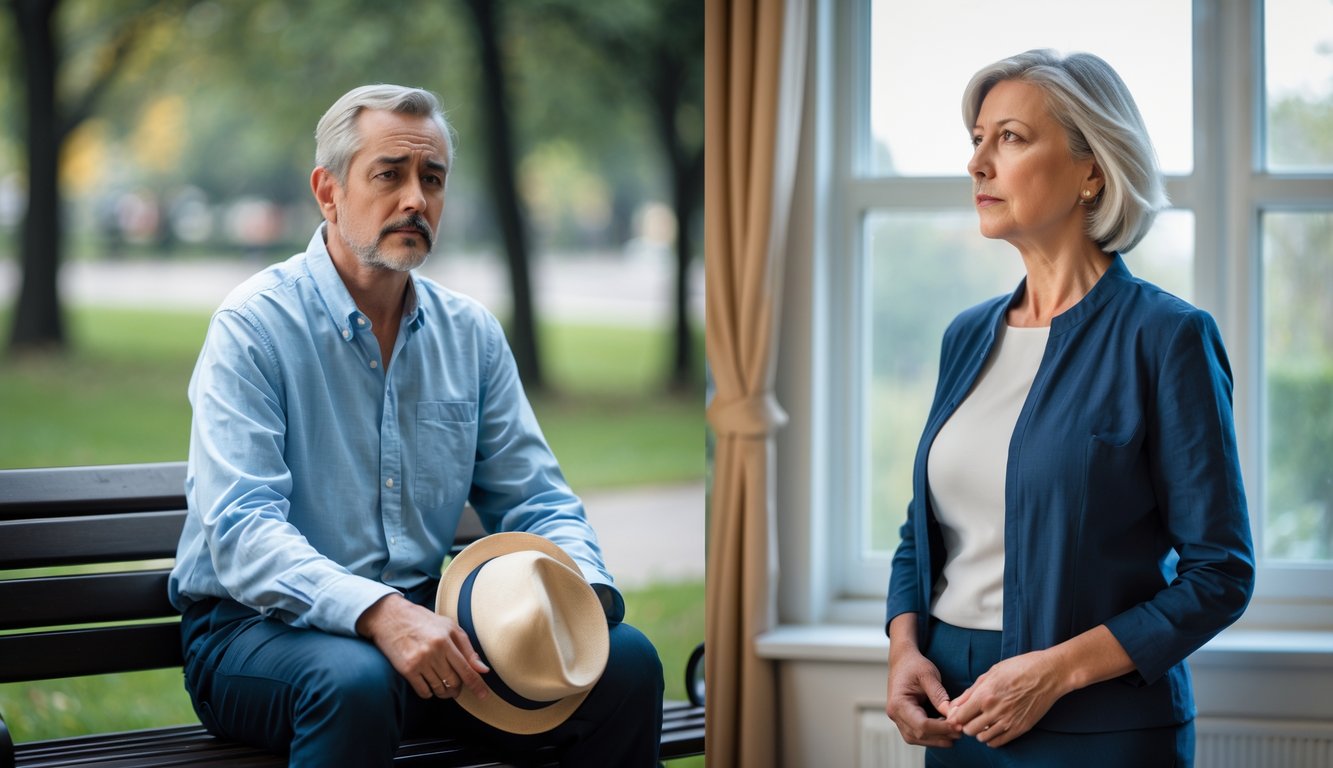

Retirement brings more than financial challenges—it triggers a fundamental identity crisis that affects men and women differently.

Research reveals that the transition from working life to retirement creates distinct psychological and social experiences based on gender, with each facing unique obstacles in redefining their sense of self and purpose.

The primary difference between men and women in retirement centers on how work connects to personal identity, with men typically experiencing more dramatic identity shifts when leaving career-focused roles.

Women often navigate complex transitions between multiple life roles including caregiving responsibilities.

This distinction influences everything from retirement timing decisions to post-career satisfaction levels.

Gender differences in retirement decisions extend beyond financial planning into deeper questions of identity, social connections, and life purpose.

Understanding these patterns helps explain why women face consistently higher levels of retirement concerns despite having similar retirement hopes as men.

Key Takeaways

- Men and women experience retirement identity crises differently based on how strongly work defines their personal identity

- Financial disparities create additional psychological stress for women who face greater retirement security challenges

- Gender-specific retirement patterns affect both individual well-being and broader social policy needs

The Gendered Nature of Retirement Identity Crisis

Men and women experience fundamentally different challenges when transitioning from work to retirement, with identity disruption varying significantly based on how each gender has historically constructed their sense of self.

Research shows that gender differences in retirement stem from distinct relationships with work identity and social role expectations.

Understanding Identity in Retirement

Identity formation during retirement depends heavily on how individuals previously defined themselves through their careers and social roles.

For many older Americans, retirement represents a major life transition that challenges long-held beliefs about personal worth and purpose.

Work-based identity traditionally plays a larger role for men, who often derive primary self-definition from professional achievements and career status.

When this central identity pillar disappears, men frequently struggle with feelings of purposelessness and diminished social value.

Women typically maintain more diverse identity sources throughout their working years.

Even career-focused women often balance professional identity with family roles, community involvement, and relationship maintenance.

| Identity Component | Men | Women |

|---|---|---|

| Primary source | Career achievement | Multiple roles |

| Social connections | Work-based | Family and community-based |

| Self-worth measures | Professional status | Relationship quality |

The importance of work to self-identity represents the primary difference between how men and women approach retirement transitions.

How Gender Influences Retirement Adjustment

Adjustment patterns differ markedly between genders due to varying coping mechanisms and social support systems.

Men often experience more dramatic identity disruption because retirement eliminates their primary source of social interaction and personal validation.

Men’s adjustment challenges include:

- Loss of workplace social networks

- Difficulty finding new sources of purpose

- Resistance to seeking emotional support

- Struggles with domestic role transitions

Women’s retirement adjustment typically involves smoother transitions due to established non-work identities.

However, women face unique financial pressures that create different stress patterns.

Research on psychological well-being in retirement reveals that women and men draw satisfaction from different sources during this life stage.

Women often find fulfillment through family relationships and community engagement.

Financial security concerns affect women disproportionately.

Lower lifetime earnings and interrupted career patterns create anxiety about retirement sustainability that men experience less frequently.

The Role of Socialization and Career Patterns

Traditional gender socialization creates distinct career patterns that directly influence retirement identity formation.

Men typically follow linear career progressions with continuous employment, while women experience more fragmented work histories due to caregiving responsibilities.

Socialization effects begin in childhood and continue throughout working years:

- Men learn to prioritize career advancement

- Women balance multiple competing priorities

- Society reinforces different success measures for each gender

Women and retirement patterns show greater diversity across different countries and cultural contexts than men’s more standardized retirement transitions.

Career interruptions for caregiving create both challenges and advantages for women entering retirement.

While financial security may be compromised, women often possess stronger caregiving skills and social networks.

Career pattern differences:

- Men: Continuous employment, higher earnings, pension accumulation

- Women: Career breaks, part-time work, reduced retirement savings

These patterns shape not only financial readiness but also psychological preparation for retirement identity reconstruction.

Key Gender Gaps Shaping Retirement

Women face retirement balances that are often 30% lower than men’s, driven by wage disparities, pension gaps, account differences, and part-time employment patterns.

These financial gaps create distinct challenges that shape how each gender experiences retirement planning and security.

The Gender Wage Gap and Its Lasting Impact

The wage gap creates compounding effects throughout a woman’s career that directly impact retirement savings.

What starts as a 20% pay gap soars to a 44% pay gap over the course of a woman’s career.

This disparity becomes magnified in retirement accounts because contributions are typically based on salary percentages.

A 6% contribution rate applied to lower wages results in smaller dollar amounts being invested over time.

Compound Interest Amplifies the Gap:

- Lower initial contributions mean less money earning returns

- Decades of reduced contributions create exponentially larger gaps

- Career interruptions for caregiving further reduce earning potential

The mathematical reality is stark.

When modeling identical 6% contribution rates and 6% annual returns, women end up with retirement balances 31% less than men by age 65.

Gender Pension Gap Explained

The gender pension gap represents the difference in retirement income between men and women from all sources.

A gender pension gap exists in virtually every country, with women receiving pensions between 25% to 30% lower than men.

This gap stems from multiple factors that accumulate over decades.

Lower lifetime earnings reduce Social Security benefits, which are calculated based on the highest 35 years of earnings.

Primary Contributors to Pension Gaps:

- Career interruptions for childcare and eldercare

- Part-time employment with limited benefits

- Lower-paying industries with fewer women in leadership roles

- Shorter tenure in jobs that offer pension benefits

Women also face unique longevity challenges.

They typically live six years longer than men but often retire earlier, around age 62 compared to men’s average retirement age of 65.

Retirement Account Disparities

Gender disparities in retirement accounts extend beyond simple balance differences to include access and participation patterns.

Women participate in 401(k) plans at equal rates as men and contribute as much, if not more, than men do when they have access.

The real issue lies in employment patterns that affect account access.

Many women work in positions or industries that don’t offer employer-sponsored retirement plans.

Key Account Disparities:

| Factor | Impact on Women |

|---|---|

| 401(k) Access | Limited in part-time and service jobs |

| IRA Contributions | Reduced due to lower disposable income |

| Employer Matching | Missed opportunities in jobs without benefits |

| Account Rollovers | More complex due to career interruptions |

Women often rely more heavily on Individual Retirement Accounts (IRAs) when employer plans aren’t available.

However, IRAs typically lack the cost advantages and employer matching benefits of workplace 401(k) plans.

Influence of Part-Time Work on Savings

Part-time employment significantly impacts retirement savings capacity and creates long-term financial disadvantages.

Women are more likely to work part-time due to caregiving responsibilities, which affects their ability to build retirement wealth.

Part-Time Work Challenges:

- No employer benefits including 401(k) plans or matching contributions

- Lower hourly wages compared to full-time equivalent positions

- Irregular income making consistent savings difficult

- Limited Social Security credits affecting future benefit calculations

Lower-paid and part-time workers, many of whom are women, miss out on workplace retirement plans entirely. This exclusion forces reliance on individual savings accounts that lack institutional support and cost efficiencies. The ripple effects extend beyond immediate savings.

Part-time workers often experience gaps in their earnings records, which directly impacts Social Security benefit calculations. Since benefits are based on the highest 35 years of earnings, years with low or no earnings reduce the final benefit amount significantly.

Decision-Making in Retirement: Men vs Women

Men and women approach retirement decisions through distinctly different lenses, with family considerations playing a predominant role for women while men focus more on career and financial factors.

Marital status creates additional complexity, influencing timing and financial strategies differently across genders.

Factors Behind Retirement Decisions

Women prioritize caregiving responsibilities when making retirement decisions.

- They frequently retire earlier than planned to care for aging parents, spouses, or grandchildren.

- Financial considerations often take a secondary role to family obligations.

- Career interruptions throughout their working years make women more flexible about retirement timing.

- Many view retirement as an opportunity to focus on relationships and personal fulfillment rather than purely financial security.

Men base retirement decisions primarily on financial readiness and career satisfaction.

- They typically follow more structured timelines aligned with pension eligibility or specific savings targets.

- Health concerns also play a significant role in their decision-making process.

- Work identity strongly influences men’s retirement timing.

- Those in leadership positions often delay retirement to maintain their professional status and earning potential.

Marital Status and Its Influence

Married couples must coordinate retirement decisions between spouses, creating unique gender-based patterns. Women married to older men often retire earlier to spend time together, while those married to younger men may work longer.

Financial planning becomes more complex for married women who may rely on spousal benefits. They must consider Social Security spousal and survivor benefits when timing their retirement.

Single women face greater financial pressure to delay retirement due to lower lifetime earnings and no spousal support system. They must build larger individual retirement funds to compensate for reduced Social Security benefits.

Divorced women encounter particular challenges, having lost years of retirement savings during career breaks and potentially losing access to spousal benefits depending on marriage duration.

Voluntary vs Involuntary Retirement Patterns

Voluntary retirement shows clear gender differences in motivation and timing. Women often retire voluntarily to pursue caregiving roles or personal interests, even when financially unprepared.

Men typically retire voluntarily only when they reach specific financial milestones. Women demonstrate more flexibility in accepting reduced income for lifestyle benefits.

They value time freedom and family connections over maximizing retirement wealth. Involuntary retirement affects men and women differently across industries and circumstances.

Men experience higher rates of involuntary retirement due to physical job demands or corporate restructuring in male-dominated fields. Women face involuntary retirement through layoffs in service industries or when caregiving demands become overwhelming.

Research shows significant gender differences in how older Americans adapt to unexpected retirement timing and financial consequences.

Social Security and Policy Impacts by Gender

Government retirement systems create distinct outcomes for men and women through benefit calculations tied to lifetime earnings patterns. Policy reforms continue addressing these disparities while maintaining system sustainability across different demographic groups.

Social Security Eligibility and Benefits

Social Security benefits reflect the persistent wage gap between genders throughout working careers. Women’s average pension income in the United States is approximately 34 percent lower than men’s due to lower lifetime earnings and career interruptions.

The benefit calculation formula bases payments on the highest 35 years of indexed earnings. Women who take career breaks for caregiving often have years with zero earnings counted in this calculation.

This reduces their Average Indexed Monthly Earnings and consequently their monthly benefits. Spousal benefits provide some protection for women with limited work histories.

A spouse can claim up to 50% of their partner’s full retirement benefit if it exceeds their own earned benefit. Survivor benefits allow widows to receive their deceased spouse’s full benefit amount.

Women typically outlive men by several years, with male life expectancy at 74.8 years compared to longer female lifespans as of 2022. This longevity difference means women rely on Social Security benefits for extended periods despite receiving lower monthly payments.

Pension Policy Reforms and Gender Neutrality

Modern pension reforms aim to eliminate gender-based distinctions while addressing structural inequalities. The shift from defined benefit to defined contribution plans affects men and women differently based on career patterns and investment behaviors.

Defined contribution plans offer increased portability, benefiting women who change jobs more frequently due to family obligations. However, these plans require individual investment decisions and provide no guaranteed lifetime income, creating risks for women’s longer retirement periods.

Key Policy Changes:

- Elimination of gender-specific mortality tables in benefit calculations

- Enhanced spousal protection in pension distributions

- Improved vesting schedules for interrupted careers

The SECURE 2.0 Act includes provisions expanding retirement plan access for part-time workers, many of whom are women. These changes allow workers with at least 500 hours annually for two consecutive years to participate in employer plans.

Gender inequality in the labor market and household responsibilities results in different social security risks and entitlements for men and women. Policy makers continue evaluating credit systems for caregiving years and minimum benefit guarantees to address these structural disparities.

Psychological and Social Effects of Gendered Retirement

Men experience retirement as a loss of professional identity and financial control, while women face complex transitions involving caregiving responsibilities and social relationship changes. These gender differences in retirement transitions create distinct psychological challenges for each group.

Identity Crisis After Leaving Work

Men typically derive significant identity from their professional roles and breadwinner status. When retirement removes these defining characteristics, they experience what researchers call identity disruption.

The transition from career-focused identity to retiree status often creates confusion about self-worth and purpose. Women’s retirement identity crisis manifests differently due to their complex role juggling throughout their careers.

Many women continue caregiving responsibilities for elderly parents or grandchildren during retirement. This creates role continuity rather than the complete identity shift men experience.

Research on gender and retirement meaning shows that work importance to self-identity varies significantly between genders. Men struggle more with the absence of professional achievement markers.

Women often view retirement as an opportunity for personal time after decades of serving others. The timing of identity adjustment differs between genders.

Men may experience immediate identity loss upon retirement. Women frequently navigate gradual transitions that blend work, family, and personal interests.

Well-Being and Mental Health Challenges

Research reveals that financial assets and job dissatisfaction are more strongly related to men’s psychological well-being in retirement compared to women. Men’s mental health depends heavily on maintaining financial security and control over resources.

Women’s psychological well-being connects more strongly to social relationships and support networks. Preretirement social contacts significantly impact women’s retirement satisfaction more than men’s.

Women who lose workplace social connections may experience isolation and depression. Depression patterns differ between retired men and women:

- Men show higher rates of depression immediately following retirement

- Women experience gradual mood changes related to relationship quality

- Social support buffers depression more effectively for women

- Financial stress creates greater psychological distress for men

Gender differences in social resources significantly influence retirement mental health outcomes. Women typically maintain stronger social networks but face greater economic vulnerability.

Men possess more financial resources but struggle with reduced social connections after leaving work environments.

Frequently Asked Questions

What are the key gender differences in experiencing a retirement identity crisis?

Men typically experience more abrupt identity shifts when leaving full-time careers, as their professional roles often define much of their social identity. They may struggle with loss of status and structured daily routines.

Women frequently face more complex identity transitions due to multiple role changes throughout their careers. Many have already navigated identity shifts related to caregiving responsibilities, making retirement adjustments feel less jarring.

Research shows that men and women experience different retirement decisions and outcomes based on how gender interacts with various life factors. This complexity means women often have more fragmented career narratives to reconcile during retirement.

How do societal gender roles impact an individual’s sense of self during retirement?

Traditional expectations that men serve as primary breadwinners can intensify identity loss when they stop working. The transition from provider to retiree may challenge deeply held beliefs about masculinity and worth.

Women who followed conventional paths as caregivers may find retirement offers new opportunities for self-discovery. Those who balanced careers with family responsibilities might experience relief from competing demands.

Changing social norms create additional complexity for both genders. Modern retirees must navigate between traditional role expectations and evolving definitions of successful aging.

Why might women face unique challenges when it comes to retirement planning and savings?

Women have just 70% of the overall retirement income that men have, creating significant financial stress during retirement years. This gap stems primarily from the gender pay gap, where women earn 83 cents for every dollar men earn.

Career interruptions for caregiving responsibilities reduce women’s ability to accumulate retirement assets. Time away from the workforce means fewer contribution years and less compound growth on investments.

Women’s retirement balances are often 30% lower than men’s despite similar participation rates in retirement plans. The pay gap compounds over time, creating substantial wealth disparities by retirement age.

In what ways does retirement affect men’s identity differently than women’s?

Men often derive significant identity from job titles and professional achievements. Retirement can trigger what psychologists call “role exit,” where former executives or professionals struggle to redefine themselves without career labels.

The loss of workplace social connections hits many men particularly hard. Without colleagues and business relationships, some experience isolation and depression during early retirement years.

Women typically maintain more diverse social networks outside of work throughout their careers. This broader social foundation often provides better support systems during retirement transitions.

How might the lower retirement age for women influence their identity and financial security?

Women tend to retire earlier at 62 while men retire around 65, creating additional financial strain. Earlier retirement means fewer earning years and reduced Social Security benefits.

The combination of lower lifetime earnings and earlier retirement creates a double financial burden. Women must stretch smaller retirement savings over longer periods due to increased longevity.

Early retirement may reflect caregiving responsibilities rather than personal choice. Many women leave the workforce to care for aging parents or spouses, limiting their financial independence.

To what extent does gender equality progress influence retirement outcomes for women?

Workplace equality gains have improved women’s access to employer-sponsored retirement plans. More women now participate in 401(k) programs at rates equal to men, though contribution amounts remain limited by salary differences.

Educational advances mean younger women enter higher-paying careers that support better retirement savings. However, the gender pay gap persists across all education levels, continuing to impact long-term wealth accumulation.

Policy changes like paid family leave and flexible work arrangements help women maintain career continuity. These developments reduce the career penalties that traditionally undermined women’s retirement security.